Gold’s Super Bull Market

Atlas Pulse Gold Report Issue 101

The gold price used to follow the bond market, yet with bonds plummeting, gold has shown resilience. In this piece, I explain why gold provides shelter from a deteriorating bond market. If bonds are the benchmark, gold is not just in a bull market but in a super bull market.

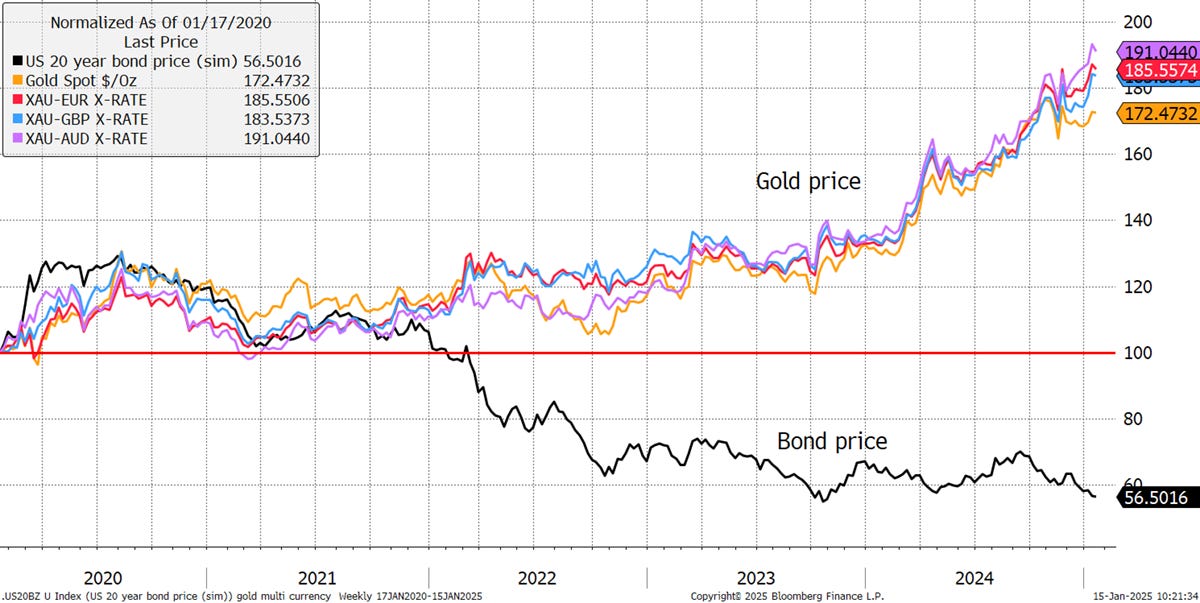

While gold is down 3.7% in USD since the October 2024 peak, gold is trading at an all-time high in pounds, Aussie, and Euro, suggesting the severity of this gold correction has been overstated. Yet the US 20-year bond has slumped by 9% and gold has shrugged much of it off.

Gold in Currencies and Bonds Since October 2024 Peak

Looking a little further back to the beginning of the pandemic, gold has risen by 72% in USD and 91% in AUD, while the 20-year constant maturity treasury has fallen by 44% on a capital return basis. You can even see how gold and the bond were trading in sync for much of 2020 and 2021.

Gold in Currencies and Bonds Since 2020

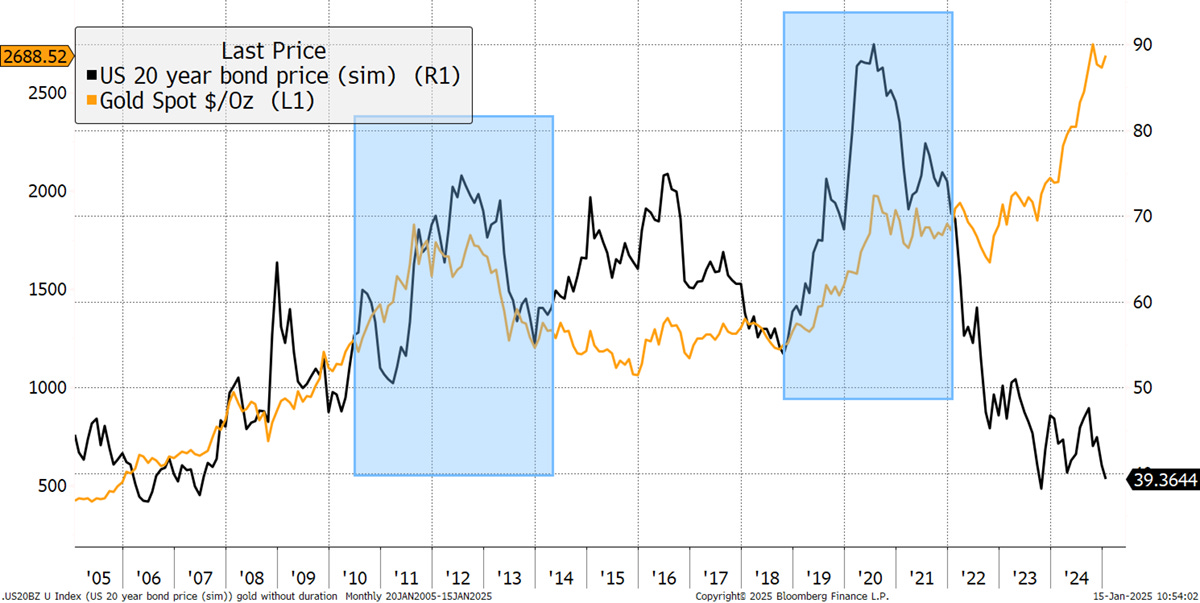

Looking back 20 years, gold and bonds moved together much of the time. There was a gold slump between 2011 and 2015 when bonds were ahead, which was largely due to the unwinding of prior exuberance and a low inflation environment. The blue squares show how the peaks in the gold price coincided with the strength in bonds. Then, in 2022, as interest rates started to rise, it was all change. The gold bull market resumed, while bonds crashed.

Gold and the Long Bond Since 2005

The standard answer is the war in Ukraine and the confiscation of Russian assets, which has boosted the demand for gold. That is no doubt true, but there is also a macroeconomic angle that is becoming increasingly apparent because what happened in the 1970s is being repeated.

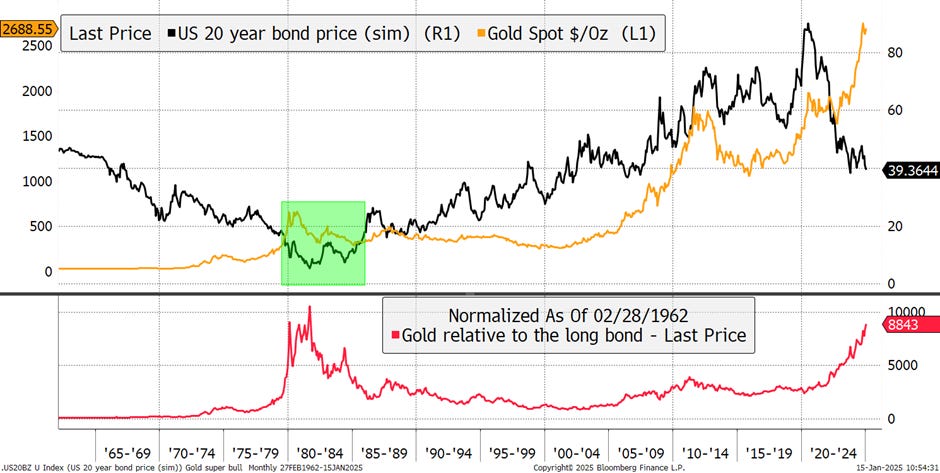

Bond yields rose after WW2, a time when interest rates were capped to support the war effort. The post-war economy grew quickly, and high levels of money supply led to an inflationary boom. When the gold standard was dropped by President Nixon in 1971, bond yields rose quickly, causing bond prices to fall. Gold was the natural antidote, and the worse bonds became, the more gold thrived.

Gold and the Long Bond Since 1960

The difference between gold and bonds is shown above in red. In the 1970s, the red line rose significantly, just as it is again today. If we examine it closely in the chart below, there are three distinctive periods:

The green patch occurred when bond yields were falling from high levels in 1980 to moderate levels in 2000. Gold was in a bear market during this period and did not perform, while bonds delivered abnormally high returns.

The blue patch is the 2000 to 2020 gold bull market with a break from 2011 to 2015. For much of that time, gold moved in sync with the bond market. In this era, gold performed strongly, while bonds performed well.

In the purple patches, gold performed strongly during times when bonds have been weak. Gold has provided a safe haven from a collapsing bond market. These are gold super bull markets.

Gold Super Bull Markets

It is notable how gold has provided different roles at different times throughout history, and it is remarkable how these regimes have changed. We are living through one of these eras when the price of gold has low sensitivity to internet rates, which is remarkable. Investors can get 4.5% for holding cash in the bank or nearly 5% in the long bond. Yet they voluntarily give up the interest on offer because they believe the cost of borrowing will continue to rise, and the rates are not high enough to offset capital losses from bonds in the long run.

Most importantly, what broke the gold Super Bull of the 1970s? The answer is peak interest rates and bond yields. You can see that in the green box two charts up. When rates peaked, it was all over for gold because peak rates signalled the system was back in control after a period of inflation, deficits and disorder. The time to sell gold will be when we can be sure the authorities are firmly back in control.

With budget deficits approaching the limits of affordability, it is hard to imagine there isn’t more to come.

21Shares ByteTree BOLD ETF (BOLD Switzerland)

Bitcoin had a strong run last year, while gold didn’t do too badly either. The BOLD ETF is up a respectable 85% in USD since its inception in April 2022. The USD shares class had a volatility of 15% last year, similar to Berkshire Hathaway, making BOLD a high Sharpe Ratio strategy. That means high returns for a modest level of price volatility.

Bitcoin, Gold and BOLD - Since Inception

I can’t find an ETF in the world with a higher Sharpe Ratio than BOLD. If you can find one, please let me know. Please visit our website, BOLD.report, for more details on the BOLD ETF.

Summary

Gold is no longer behaving like a bond, and that is important. Those seeking to diversify away from bonds are not only the central banks, but asset allocators who believe this era of debt and deficits has further to run.

Thank you for reading Atlas Pulse. The Gold Dial remains in Bull Market.

Charlie Morris is the Founder and Editor of the Atlas Pulse Gold Report, established in 2012. His pioneering gold valuation model, developed in 2012, was published by the London Mastels Bullion Association (LBMA) and the World Gold Council (WGC). It is widely regarded as a major contribution to understanding the behaviour of the gold price.

We would love to hear your feedback, so please share your thoughts in the comments below or contact Charlie at charlie.morris@bytetree.com. It would really help us if you could like, restack/share this update and subscribe to our Substack. Thank you so much for your support!